Introduction

Offshore wind has many advantages to onshore wind, including less variability in wind speeds, more wind hours, and often higher acceptance for wind parks by local communities, especially if those parks are far offshore.

But where is the industry today? What are the costs and technical challenges? How are oil and gas companies involved in the expansion of offshore wind? And where is offshore wind heading?

Advantages

Full load hours for offshore wind turbines (WTG) can reach up to 5,200 hours per year, significantly higher than the 3,700 annual hours for onshore WTG, or the 2,300 annual hours for PV (1). In percentage terms this means that offshore WTG can produce at its rated capacity almost 60% of the time, while onshore WTG and PV achieve this only up to 42 and 26% of the time.

Higher wind availability and the ability to construct turbines at larger distances to human settlements make it possible and financially viable to install larger WTG offshore than onshore. Furthermore, if the appropriate vessels are available, it is easier to transport large WTG parts by sea, as there are no roads, forests, or traffic to consider. In Europe, the average rated capacity of offshore WTG installed in 2019 was 8.2 MW, significantly larger than the average 3.3 MW for onshore WTG in the same year (2). In Germany the trend in 2020 was similar: onshore WTG averaged 3.4 MW, while their offshore counterparts doubled this capacity, averaging 6.8 MW per turbine. While these are already large capacities, this is by no means the end of the expansion. In 2020 GE Renewable Energy received the certification necessary to start deploying its 12 MW Haliade-X turbines, quickly followed by a 13 MW version in January of 2021. Over the past year Vestas and Siemens both launched 15 MW turbines, expecting them to be installed at a commercial scale by 2024 (3,4). Chinese wind turbine producer MingYang Smart Energy raised this capacity as it recently released details of its newest turbine, also expected to be installed by 2024 and rated at 16 MW (5).

Furthermore, stabler wind conditions lead to higher predictability of produced electricity, something that is dearly desired by grid operators as electricity production shifts towards more renewable energy sources, which are much more intermittent than other sources of energy.

Size of the market

In its 2021 World Energy Transition Outlook the International Renewable Energy Agency (IRENA) laid out pathways to keeping global warming to 1.5° C, as agreed upon in the Paris Climate Agreement (6). In the report, as well a subsequent publication about offshore renewable energy, the agency estimates a need for 2,000 GW of offshore wind to be deployed by 2050 to achieve the agreed-upon goals (7).Figure 1 gives an overview of historically installed offshore wind capacity, as well as how the 2,000 GW by 2050 could be split by regions, based on a market intelligence report by the Global Wind Energy Council (8).The estimated interim goals are an installed capacity of 382 GW by 2030 and 1,129 GW by 2040, shining a light on how quick and exponential an expansion of the sector has to take place.

| Country/Area | 2000 | 2005 | 2010 | 2015 | 2018 | 2019 | 2020 | 2050 |

| Europe | 67 | 684 | 2.931 | 10.996 | 18.763 | 22.031 | 24.837 | 640.000 |

| North America | – | – | – | – | 29 | 29 | 42 | 360.000 |

| Asia | – | 1 | 125 | 722 | 4.833 | 6.295 | 10.414 | 760.000 |

| Latin America | – | – | – | – | – | – | – | 120.000 |

| Pacific | – | – | – | – | – | – | – | 80.000 |

| Africa / Middle East | – | – | – | – | – | – | – | 40.000 |

| Worldwide | 67 | 686 | 3.056 | 11.717 | 23.626 | 28.355 | 35.293 | 2.000.000 |

Figure 1: Historical and potential installed offshore wind capacity by region (rounded; in MW)

Costs

According to the IRENA, the levelised cost of electricity (LCOE) for offshore wind energy fell from 16.1 US dollars (USD) in 2010 to 8.4 USD per MWh in 2019. For the year 2023 IRENA expects the average auction price for offshore wind energy to fall between 5-10 USD per MWh. However, even the lower end of this expected range is still above the average worldwide auction price for onshore wind energy in 2020, which was approximately 4.5 USD per MWh (9).

One driver of the falling overall costs is the cost of installing wind turbines, which decreased rapidly over the recent years. While the global average cost per installed MW capacity peaked at 5.4 million euros in 2011, it fell to 3.2 million euros by 2020. Further, due to the still smaller market size than onshore wind or PV, the average installation prices are much more volatile from year to year, as individual projects have a higher overall impact on the global average cost. This adds to explain the low average costs of 2020, as deployment was driven by China and the Netherlands, both of which have publicly supplied grid connections, reducing electrical infrastructure costs. The resulting, relatively low price of less than €3 m per MW capacity (10) then serves to decrease the global mean.

Financing costs have also dropped significantly, as more projects have been commissioned and lenders are starting to get a better understanding of offshore wind energy generation. The spread between financing costs over the risk-free interest rate provides an overall image of how risky investors deem projects to be. While the sample size is still small, for offshore wind projects in Europe this spread has halved between 2010 and 2019 (11).

Another area which has already contributed to lowering overall costs and will continue to do so is operation and maintenance (O&M). There are two main reasons why O&M costs for offshore wind parks are high. One is the long distances the vessels must travel to reach the individual parks. Driving cost reductions here are economies of scale. As more wind parks are being built, offshore vessels can attend to larger clusters, reducing the distances travelled per job, and ultimately saving costs. The growing size of wind turbines drives down the costs of maintenance even further, as the same amount of generating capacity can be spread across less turbines.

A second O&M cost component is more specific to floating wind turbines and relates to the constantly moving sea. Onshore wind turbines can be reached via a steady ground and fixed-bottom offshore parks are usually in depths where the vessels drop steel legs into the ground, giving them a stable environment to work from. Floating offshore wind turbines are in depths where this is no longer possible, making it necessary to perform maintenance from moving ships. To further complicate the matter, the turbines themselves are moving as well (12).

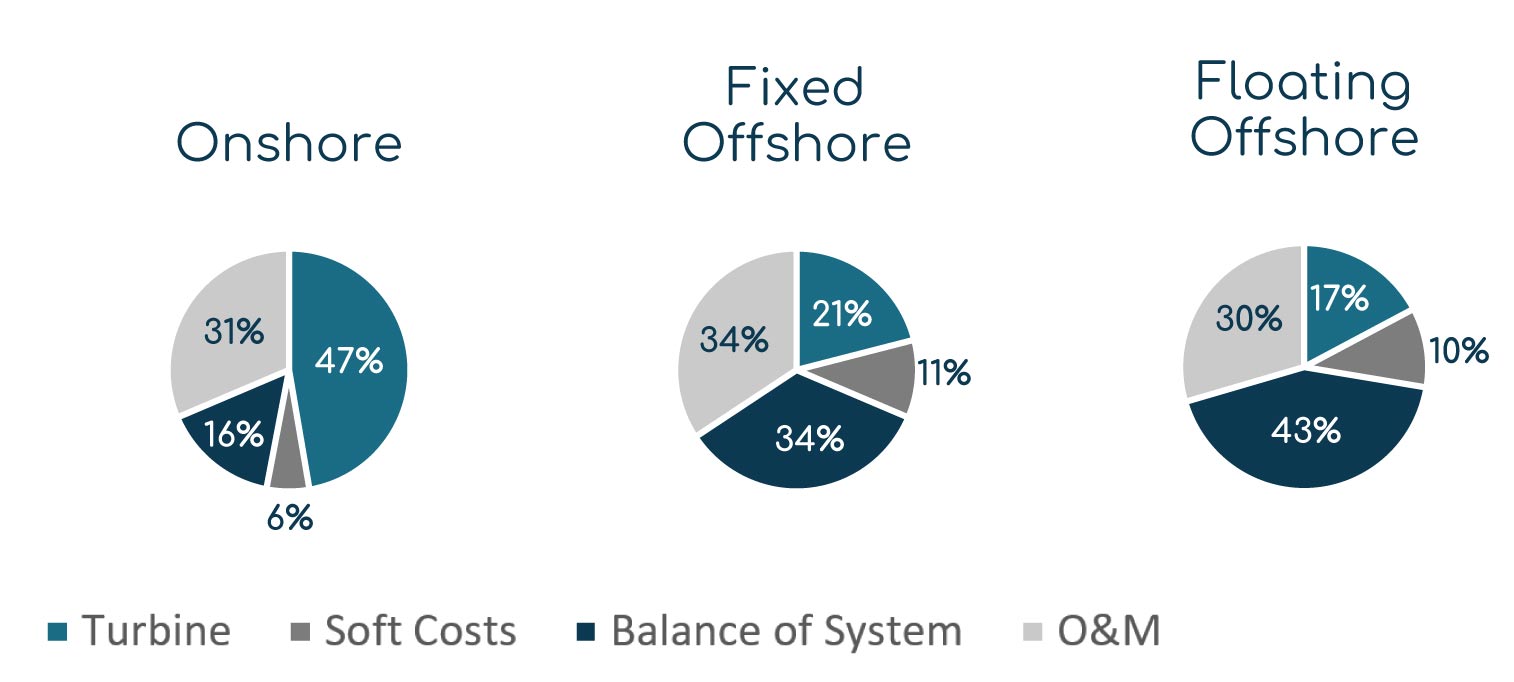

An overview of how different the cost structures of wind projects can be, comes from reference projects by the NREL. While almost 50% of the total cost of an onshore project is made up of the turbine price, the share for offshore projects is significantly lower, at around 20% of the total costs. The reason for that lower percentage is obviously not the usage of cheaper turbines offshore. Rather, it is the increased total project cost due to much higher ‘balance of the system’ costs, which almost entirely consist of higher costs for substructures and foundations, electrical infrastructure, and assembly and installation. Figure 2 gives an overview of the differences in cost structure by wind technology.

Figure 2: Cost structures by type of wind energy project (13)

As mentioned before, grid connection poses a large cost for offshore wind farms. Cables must be laid under water over large distances and substations have to be built out at sea. This infrastructure does not only need to be built between the wind farms and shore, but inter-array as well, connecting the individual turbines to the substation. A recent example of how complicated and expensive offshore grid connections can be comes from industry-leader Ørsted. Cables at their 580 MW Race Bank wind park, situated 27 km off the coast of England, were found to be faulty due to movement on the scour protection. Ørsted is now planning on placing large rocks on the cables to keep them from moving and eroding. The company has done this in previous offshore projects and believes it to be a viable solution to the problem. However, the damage at Race Bank is done and Ørsted estimates the associated costs to be up to €400m (14). According to the international renewable energy insurance expert GCube the most frequent faulty component types of an offshore wind farm are the export cable, the foundation, and the inter-array cable. While the loss severity of inter-array cables can be quite high, as exemplified by Race Bank, GCube estimates it to be only about half as much as the loss severity from export cables and only about one third of foundation problems (15).

Europe

In 2020 half of the 2.9 GW new offshore wind capacity was installed in the Netherlands, while the UK remained the country with the largest installed capacity, being home to more than 10 of the 25 GW installed in Europe, followed by Germany with 7.7 GW and the Netherlands with 2.6 GW (16).

In its strategic outlook the European Commission set goals of 60 GW for the year 2030 and a total of 300 GW installed capacity by 2050 (17).

Germany

At the end of 2020 more than 1 GW of wind turbine capacity was connected to the grid in the Baltic Sea, while more than 6 GW were installed in the North Sea. In total this amounted to 1,501 wind turbines installed in German waters. Contracts had been awarded for almost 3 GW of further capacity to be commissioned by the end of 2025. With the amendments to the German Offshore Wind Energy Act (WindSeeG) from December 2020 the goals for installed offshore wind capacity were lifted from 15 to 20 GW by 2030 and to 40 GW by 2040 (19).

The potential for offshore wind in Germany remains large, but to reach the goals of 2030 and 2040 there must be a steep rise in annual installations. Positive indications are the results from the offshore wind tender of September 1, 2021. Three areas, with a total potential of almost 1 GW, were raffled to RWE and EDF, as ‘most bidders’ bid at zero cent prices. The background here is that the EEG leads to an entitlement to a grid connection to the mainland and the right to operate the offshore farms for 25 years (19).

A considerable problem Germany is currently facing is the geographically uneven distribution of electricity generation and consumption. Windier regions in the North have led to a bigger presence of turbines and electricity generation, while a lot of demand is located in southern regions (20). The expansion of the offshore sector will complicate this matter further, as the entire offshore potential is located to the north of the country. Instead of having spillovers into other markets, where Germany has even paid for foreign wind farms to be shut down in the past (21), an option of using offshore energy is by producing green hydrogen, a topic which is discussed later in the article.

United Kingdom

The United Kingdom is currently the largest offshore market in the world, with already more than 10 GW of installed capacity. As an early mover the UK already reached 1 GW of installed capacity in 2009 (22). Since 2015 the Crown Estate, which owns the rights to the seabed around the UK, has been holding auctions for leases. A novelty in 2021 has been a changed auction system, which makes investors pay an annual option fee until they get the final planning permission. This new system is not without critics, concerned that it raises costs for developers, which will eventually be passed on to consumers. As the last previous auction took place in 2010 and there is currently no date set for the next round of auctions, the 8 GW made available during 2021 appear too small to enable the national goal of 40 GW installed by 2030 (23).

Iberia

Much like the western coast of the United States, Portugal and Spain have a deep offshore seabed, which makes fixed-bottom offshore wind not a viable option to build. However, high electricity prices, which even prompted Spanish leaders to call on the EU to back measures limiting them, show a need for a rapid expansion of electricity capacity (24). With nearly 7,000 km of coastline between the two countries, developing an offshore wind sector has a significant contribution potential. A recent study by the University of Sevilla, together with the University of South-Eastern Norway, estimated that each MWh of offshore wind energy introduced into the market would drive a cost reduction of 45 euros, or about 50 % of current prices (25).

In 2020 Portugal became the first country in continental Europe with a functioning floating offshore wind park. While many countries around Europe have been running experiments over the past few years, the WindFloat Atlantic project, which has three Vestas turbines totalling 25 MW and is located 20 km off the coast, became the largest floating offshore wind project in the world (26).

China

By the end of 2020 China had installed nearly 10 GW of offshore wind capacity, overtaking Germany as the second largest offshore wind market in the world, and trailing only the United Kingdom by a small margin. In 2020 alone China installed more than 3 GW of capacity, and 2021 is expected to be another record-breaking year, as the current feed-in-tariff expires at the end of the year (27). Mid 2021 the second phase of the Yangjiang Shapa started producing energy, making it the first offshore wind farm with a capacity surpassing 1 GW in China (28).

While it is expected that China will maintain a market share in the Asian offshore market of over 70 %, how much the sector will grow depends on subsidies provided by provincial governments (29).

United States

The technical potential of offshore wind energy resources is estimated to be bigger than 2,000 GW, or nearly double the nation’s current electricity use. As of 2021 virtually none of this potential is being harnessed, as there are only two offshore wind parks with a total capacity of 42 MW commissioned (30).

However, it appears that the industry is ready to take off. After long environmental assessments of projects, 2021 saw the 800 MW Vineyard Wind project receive final permitting (31). A further eleven projects are currently in the permitting phase and the total US offshore pipeline is nearly 29 GW (32).

This charge is being led by 8 states along the eastern coast, spanning from Virginia in the South all the way up to Maine. Each of those states has set ambitious goals for the build-out of offshore wind. By 2035 New York has set a target of 9 GW of offshore wind, New Jersey has a target of 7.5 GW and Massachusetts set its target at 3.2 GW (33). This is especially impressive when considering that, as recently as 2018, state-set targets for the entire US totaled 9.1 GW (34).

Due to the deeper waters along the west coast offshore wind is currently less developed than on the east coast as wind parks there will have to be floating, rather than ground mounted. However, California is planning its first auctions for two seabed leases along its coast in 2022, as the California SB 100 Joint Agency Report found that at least 10 GW of offshore wind capacity will be needed to meet its target of 100 % clean energy by 2045 (35).

Lower average wind speeds lead to less attractive offshore wind projects in the Gulf of Mexico (36). Still, since a lot of oil and gas exploration has been done in the Gulf of Mexico oil majors have a large presence there.

Oil Majors

Whether they are positioning themselves to be offshore wind developers, such as Equinor, or are more oriented towards providing leadership along the entire green energy pipeline, such as Shell or BP, oil companies are trying to transform their identities. Together with goals of lowering their carbon emissions companies have set astonishing goals for renewable energy capacities in their portfolios. Examples include BP, which is working towards 50 GW by 2030 and TotalEnergies, with a goal of 100 GW by 2030. A lot of work remains to be done, as those two companies currently only hold around 10 GW of renewable capacity combined (37,38).

While those portfolios will ultimately consist of a range of renewable energy technologies, offshore wind is being pursued by almost all big oil companies. Skills and knowledge in working large engineering projects, as well as working offshore projects, make oil majors convinced they can prove to be competitive. A report by the IEA found that up to 40 % of the costs for offshore wind overlap with oil industry costs (39).

While there are differences in how long companies have been involved in offshore wind projects, and whether they are backing fixed-bottom or floating technologies, one thing is clear – oil companies have arrived in the offshore wind sector, and in a big way.

Critics of the oil majors’ entrance into the offshore wind market, to no surprise, include other developers. They claim that the oil majors, which often have cash filled pockets, are driving up the costs of seabed leases, ousting more experienced developers. Pressured to keep other costs low, suppliers and contractors are chosen by price, rather than merit (40). As most offshore developers are utilities, too large to be bought by the oil companies, strategic partnerships are being formed, such as EnBW and BP, developing offshore projects together (41).

One illustrating finding regarding this comes from the auctions for seabed leases by the Bureau of Ocean Energy Management (BOEM) in the US. In 2015, the BOEM held four auctions for seabed rights, each drawing 2-3 unique bidders. Early movers like Ørsted and Iberdrola won these auctions and paid an average of 827 USD per km2 for 2,825 km2. When three auctions, totaling 1,572 km2, took place in 2018 each auction had 11 unique bidders. The winners of the auctions, which included two major European oil companies, paid an average price of 257,500 USD per km2, more than 300 times the average value of the 2015 auctions (42). How much of this increase is due to the oil majors entering the market, as well as which costs and benefits arise from increased competition is beyond the scope of this article.

What is certain is that the oil companies also have the knowledge and equipment to handle liquids and gasses like hydrogen.

Green Hydrogen

High wind speeds, many wind hours, and the potential to install large turbines all lead to high electricity production, a necessity to produce green hydrogen. The only other ‘ingredient’ needed for hydrogen production is water, of which there is plenty in the sea. Around the world, different developers are working on projects which would desalinate the seawater and then use it to produce green hydrogen on offshore structures. Transportation to shore can then take place via pipelines or specialised ships.

In Germany H2Mare is one of three large-scale hydrogen projects supported by the federal government. H2Mare is experimenting with using offshore wind energy to create green hydrogen and is being coordinated by Siemens, which is planning on investing €120 m over a five-year horizon and hoping to have a functioning demonstration plant by 2026 (43).

Bringing knowledge of working offshore projects and the handling of gasses, as well as a dire need to adapt their business-model to stay relevant in a changing environment, oil majors are looking at producing green hydrogen and to offshore wind farms.

Summary

In summary, the case for offshore wind energy is clear. Superb wind conditions, less impact on the human environment and the proximity to large metropolitan areas in need of electricity along coasts all around the world are just a few reasons why offshore wind is destined to take off.

As the industry grows, so will the knowledge deriving from projects. Factors such as the effects on wildlife are not yet completely certain. While many studies on the influence on birds, bats and aquatic life have been done, the relatively young age of the industry leads to partially unclear results. Challenges unique to offshore wind include the noise effects on whales during construction. Other challenges are shared with onshore wind, such as the threat to birds. However, some studies already suggest that the higher turbines offshore leave more room for birds to fly beneath the blades and remain unharmed (44).

The industry is in varying stages of development around the world, and each region is dealing with its own challenges. One thing all regions have in common is the need for increased renewable energy supply and large targets to achieve by 2030 and 2050. To fulfil these goals offshore wind will be a necessary source, wherever possible. As more and more offshore WTG are built the costs of doing so will decrease further, providing consumers with cheaper clean electricity or green hydrogen.

References:

(1) Agora Energiewende (2020): Making the Most of Offshore Wind Available at https://www.agora-energiewende.de/en/publications/making-the-most-of-offshore-wind/ (retrieved on: 24.08.2021)

(2) WindEurope (2021): Wind energy in Europe2020 Statistics and the outlook for 2021-2025 Available at: https://windeurope.org/intelligence-platform/product/wind-energy-in-europe-in-2020-trends-and-statistics/ (retrieved on: 24.08.2021)

(3) Cleanthinking.de (2021): Größte Turbine: Siemens Gamesa zeigt Zukunft der Offshore-Windenergie https://www.cleanthinking.de/grossste-turbine-siemens-gamesa-zukunft-offshore-windenergie/ (retrieved on: 24.08.2021)

(4) Windkraft Journal (2021): Vestas bringt neue Offshore-Turbine mit 15 MW auf den Markt Available at: https://www.windkraft-journal.de/2021/02/10/vestas-bringt-neue-offshore-turbine-mit-15-mw-auf-den-markt/158154 (retrieved on: 18.08.2021)

(5) CNBC (2021): Chinese firm announces giant 264-meter tall offshore wind turbine https://www.cnbc.com/2021/08/23/chinese-firm-announces-giant-264-meter-tall-offshore-wind-turbine.html (retrieved on: 24.08.2021)

(6) IRENA (2021): World Energy Transitions Outlook: 1.5°C Pathway Available at: https://www.irena.org/publications/2021/Jun/World-Energy-Transitions-Outlook (retrieved on: 23.08.2021)

(7) IRENA (2021): OFFSHORE RENEWABLES Available at: https://irena.org/-/media/Files/IRENA/Agency/Publication/2021/Jul/IRENA_G20_Offshore_renewables_2021.pdf (retrieved on: 23.08.2021)

(8) GWEC (2021): Offshore Wind Available at: https://gwec.net/offshore-wind/ (retrieved on: 23.08.2021)

(9) IRENA (2021): RENEWABLE POWER GENERATION COSTS IN 2020. Available at: https://www.irena.org/publications/2021/Jun/Renewable-Power-Costs-in-2020 (retrieved on: 18.08.2021)

(10) IRENA (2021): RENEWABLE POWER GENERATION COSTS IN 2020. Available at: https://www.irena.org/publications/2021/Jun/Renewable-Power-Costs-in-2020 (retrieved on: 18.08.2021)

(11) WindEurope (2021): Financing and investment trends 2020 Available at: https://windeurope.org/intelligence-platform/product/financing-and-investment-trends-2020/ (retrieved on: 25.08.2021)

(12) The Economist (2021): Floating wind turbines could rise to great heights Available at: https://www.economist.com/science-and-technology/2021/07/21/floating-wind-turbines-could-rise-to-great-heights (retrieved on: 23.08.2021)

(13) NREL (2020): 2019 Cost of Wind Energy Review Available at: https://www.nrel.gov/docs/fy21osti/78471.pdf (retrieved on: 25.08.2021)

(14) OffshoreWind.biz (2021): Inter-Array Cable Issue to Leave EUR 403 Million Mark on Ørsted Available at: https://www.offshorewind.biz/2021/04/29/inter-array-cable-issue-to-leave-eur-403-million-mark-on-orsted/ (retrieved on: 20.08.2021)

(15) GCube Insurance (2021): Offshore Wind Needs to Mitigate Supply Chain Risks to Ensure Longevity of Sector Available at: https://www.offshorewind.biz/2021/04/15/gcube-insurance-offshore-wind-needs-to-mitigate-supply-chain-risks-to-ensure-longevity-of-sector/ (retrieved on: 20.08.2021)

(16) WindEurope (2021): Offshore Wind in Europe – Key trends and statistics 2020. Available at: https://windeurope.org/intelligence-platform/product/offshore-wind-in-europe-key-trends-and-statistics-2020/ (retrieved on: 18.08.2021)

(17) European Commission (2020): Boosting Offshore Renewable Energy for a Climate Neutral Europe. Available at: https://ec.europa.eu/commission/presscorner/detail/en/IP_20_2096 (retrieved on: 18.08.2021)

(18) Bundesamt für Justiz (2020): Gesetz zur Entwicklung und Förderung der Windenergie auf See. Available at:https://www.gesetze-im-internet.de/windseeg.html (retrieved on: 18.08.2021)

(19) Energie & Management (2021): Noch ein Gigawatt Offshore kommt förderfrei hinzu. Available at: https://www.energie-und-management.de/nachrichten/erneuerbare/detail/noch-ein-gigawatt-offshore-kommt-foerderfrei-hinzu-144888 (retrieved on: 10.09.2021)

(20) Agora Energiewende (2020): The German Power Market: State of Affairs in 2019. Available at: https://www.agora-energiewende.de/en/publications/the-german-power-market-state-of-affairs-in-2019/ (retrieved on: 26.08.2021)

(21) GreentechMedia (2020): Germany’s Maxed-Out Grid Is Causing Trouble Across Europe. Available at: https://www.greentechmedia.com/articles/read/germanys-stressed-grid-is-causing-trouble-across-europe (retrieved on: 26.08.2021)

(22) Renewable UK (2021: Wind Energy Statistics. Available at: https://www.renewableuk.com/page/UKWEDhome (retrieved on: 25.08.2021)

(23) WindEurope (2021): Latest UK seabed leasing risks raising costs of offshore wind. Available at: https://windeurope.org/newsroom/press-releases/latest-uk-seabed-leasing-risks-raising-costs-of-offshore-wind/ (retrieved on: 25.08.2021)

(24) Financial Times: Spain urges EU to act on soaring energy prices. Available at: https://www.ft.com/content/7cf9a7c1-a103-4923-bb5b-bad93d32ca39 (retrieved on: 18.08.2021)

(25) MDPI (2021): Impact of Spanish Offshore Wind Generation in the Iberian Electricity Market: Potential Savings and Policy Implications. Available at: https://www.mdpi.com/1996-1073/14/15/4481 (retrieved on: 20.08.2021)

(26) Reve (2020): Full power at first floating wind energy project in continental Europe. Available at: https://www.evwind.es/2020/07/28/full-power-at-first-floating-wind-energy-project-in-continental-europe/76075 (retrieved on: 23.08.2021)

(27) GWEC (2021): China installed half of new global offshore wind capacity during 2020 in record year. Available at: https://gwec.net/china-installed-half-of-new-global-offshore-wind-capacity-during-2020-in-record-year/ (retrieved on: 23.08.2021)

(28) offshoreWindbiz (2021): China Gets Its First Gigawatt-Range Offshore Wind Farm. Available at: https://www.offshorewind.biz/2021/07/23/china-gets-its-first-gigawatt-range-offshore-wind-farm/ (retrieved on: 25.08.2021)

(29) GWEC Offshore Wind. Available at: https://gwec.net/offshore-wind/ (retrieved on: 25.08.2021)

(30) American Clean Power Association (2021): U.S. Offshore Wind Industry FactSheet. Available at: https://cleanpower.org/wp-content/uploads/2021/02/ACP_FactSheet-Offshore_8.5.pdf (retrieved on: 18.08.2021)

(31) Vineyard Wind (2021): Permitting. Available at: https://www.vineyardwind.com/vw1-permitting (retrieved on: 25.08.2021)

(32) Windexchange (2021): Offshore Wind Energy. Available at: https://windexchange.energy.gov/markets/offshore (retrieved on: 25.08.2021)

(33) American Clean Power Association (2021): U.S. Offshore Wind Industry FactSheet. Available at: https://cleanpower.org/wp-content/uploads/2021/02/ACP_FactSheet-Offshore_8.5.pdf (retrieved on: 18.08.2021)

(34) American Wind Energy Association (2020): U.S. OFFSHORE WIND POWER ECONOMIC IMPACT ASSESSMENT. Available at: https://static1.squarespace.com/static/5d87dc688ef6cb38a6767f97/t/5e6fad34a5ae164794dbb5f2/1584377149231/AWEA_Offshore-Wind-Economic-ImpactsV3+%28Mar+2020%29.pdf (retrieved on: 18.08.2021)

(35) California Energy Commission (2021): SB 100 Joint Agency Report. Available at: https://www.energy.ca.gov/sb100 (retrieved on: 18.08.2021)

(36) Global Wind Atlas. Available at: https://globalwindatlas.info/ (retrieved on: 23.08.2021)

(37) BP (2021): Gas and low carbon energy. Available at: https://www.bp.com/en/global/corporate/what-we-do/gas-and-low-carbon-energy.html (retrieved on: 25.08.2021)

(38) TotalEnergies (2021): Solar and Wind. Available at: https://totalenergies.com/energy-expertise/exploration-production/renewable-energies/solar-energy-and-wind-energy (retrieved on: 25.08.2021)

(39) IEA (2020): Offshore Wind Outlook 2019. Available at: https://www.iea.org/reports/offshore-wind-outlook-2019 (retrieved on: 23.08.2021)

(40) Recharge News (2021): ‘Big Oil’s push into offshore wind could threaten the long-term viability of the sector’ Available at: https://www.rechargenews.com/wind/big-oils-push-into-offshore-wind-could-threaten-the-long-term-viability-of-the-sector/2-1-989769 (retrieved on: 20.08.2021)

(41) Süddeutsche (2021): EnBW und BP: Gemeinsame Offshore-Windparks in Großbritannien. Available at: https://www.sueddeutsche.de/wirtschaft/energie-stuttgart-enbw-und-bp-gemeinsame-offshore-windparks-in-grossbritannien-dpa.urn-newsml-dpa-com-20090101-210208-99-347173 (retrieved on: 25.08.2021)

(42) BOEM (2021): Lease and Grant Information. Available at: https://www.boem.gov/renewable-energy/lease-and-grant-information (retrieved on: 25.08.2021)

(43) Siemens Energy (2021): Siemens Gamesa und Siemens Energy wollen Produktion grünen Wasserstoffs mit Offshore-Wind vorantreiben. Available at: https://press.siemens-energy.com/global/de/pressemitteilung/siemens-gamesa-und-siemens-energy-wollen-produktion-gruenen-wasserstoffs-mit (retrieved on: 27.08.2021)

(44) EcoWatch (2021): Offshore Wind Power Is Ready to Boom. Here’s What That Means for Wildlife. Available at: https://www.ecowatch.com/offshore-wind-power-and-wildlife-2649970581.html (retrieved on: 31.08.2021)